The Internal Revenue Service issued a consumer alert today following ongoing concerns about a series of tax scams and inaccurate social media advice that led thousands of taxpayers to file inflated refund claims during the past tax season.

The IRS warned taxpayers not to fall for these scams centered around the Fuel Tax Credit, the Sick and Family Leave Credit and household employment taxes. The IRS has seen thousands of dubious claims come in where it appears taxpayers are claiming credits for which they are not eligible, leading to refunds being delayed and the need for taxpayers to show they have legitimate documentation to support these claims.

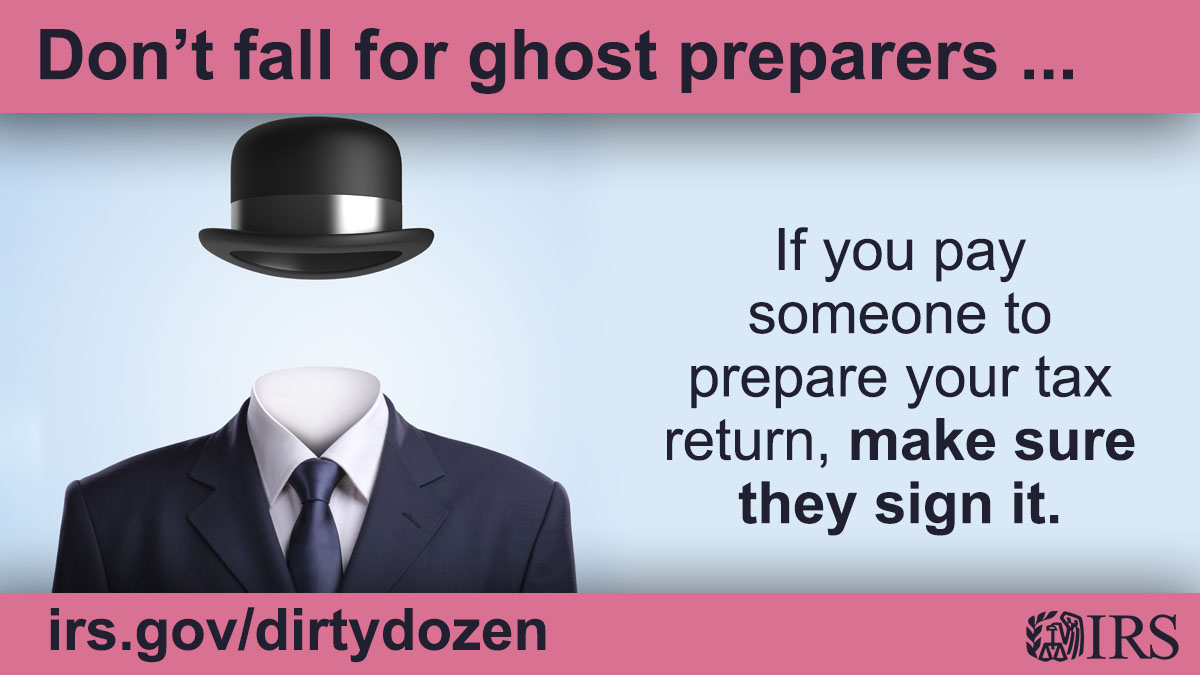

The IRS continues to urge taxpayers to avoid these scams as myths continue to persist that these are ways to obtain a huge refund. Many of these scams were highlighted during this spring’s annual Dirty Dozen series, including the Fuel Tax Credit scam, bad social media advice and “ghost preparers.”

For taxpayers who did fall for these traps, they need to follow steps to verify their eligibility for the claim. Some taxpayers could also face steep financial penalties, potential follow-up audits or criminal action for improper claims. The IRS encourages people to review the guidelines, talk to a trusted tax preparer and, in some cases, file an amended return to remove claims for which they’re ineligible to avoid potential penalties.

“Scam artists and social media posts have perpetuated a number of false and misleading claims that have tricked well-meaning taxpayers into believing they’re entitled to big, windfall tax refunds,” said IRS Commissioner Danny Werfel. “These bad claims have been caught during our fraud review process. Taxpayers who filed these claims should realize they’ve been tricked, and they face an extensive review process and a long potential wait if they’re owed a refund for other things.”

Problem claims involve Fuel Tax Credit, Sick and Family Leave Credit, household employment taxes

The IRS has identified three common themes that continue to pop up among these bad refund claims. They involve legitimate tax provisions, but they are limited to very specialized situations. The vast majority of the related claims coming in do not qualify:

Fuel Tax Credit: This specialized credit is designed for off-highway business and farming use. Taxpayers need a business purpose and a qualifying business activity such as running a farm or purchasing aviation gasoline to be eligible for the credit. Most taxpayers don’t qualify for this credit.

Credits for Sick Leave and Family Leave: This specialized credit is available for self-employed individuals for 2020 and 2021 during the pandemic; the credit is not available for 2023 tax returns. The IRS is seeing repeated instances where taxpayers are incorrectly using Form 7202, Credits for Sick Leave and Family Leave for Certain Self-Employed Individuals, to incorrectly claim a credit based on income earned as an employee and not as a self-employed individual.

Household employment taxes: Taxpayers “invent” fictional household employees and then file Schedule H (Form 1040), Household Employment Taxes, to claim a refund based on false sick and family medical leave wages they never paid.

“These improper claims have been fueled by social media and people sharing bad advice,” Werfel said. “Scam artists constantly prey on people’s hopes and try to use the complexity of the tax system to convince people there are secret ways to get a big refund. These three credits illustrate that it’s important to carefully review the tax return for accuracy before filing and rely on the advice of a trusted tax professional, not some fly-by-night preparer or a questionable source they hear on social media.”

Potentially fraudulent refunds frozen; improper claims could face follow-up compliance action

Given the questionable nature of many of these claims, the IRS has frozen the refunds for these taxpayers. Taxpayers have to follow several specific steps to resolve these issues.

Taxpayers whose refunds have been frozen will generally receive one of several letters from the IRS asking for additional information.

Initially, taxpayers may have received a letter asking them to verify their identity. In these situations, if they filed the return in question, they should review whether their tax return is accurate. For example, did they actually qualify for one of the three credits listed above? Or if they used a tax preparer, check to see if the preparer actually signed the tax return. When tax preparers don’t sign a tax return, it is a red flag that the taxpayer is being misled.

Taxpayers who improperly claimed these credits do not need to visit a Taxpayer Assistance Center (TAC) to verify their identity. However, they may need to amend their tax return to remove the improperly claimed credit.

Taxpayers should use the IRS.gov tool Should I file an amended return? to determine if they should amend their return. If they submit an amended return, they do not need to visit a TAC.

A number of taxpayers who initially received correspondence asking about their identity may be receiving an additional letter seeking additional documentation to show they actually qualify for the credits they claimed. Taxpayers who verified their identity in-person may receive these letters. Taxpayers who haven’t verified their identity yet and receive one of these letters asking for additional documentation should follow the advice on the most recent letter.

These letters – IRS Notice 3176c – apply to potentially frivolous tax returns, which includes incorrect claims for Fuel Tax Credits, Sick and Family Leave Credits and household employment taxes.

Legitimate taxpayers qualifying for these credits can submit documentation showing they actually qualify for the credit. But people who don’t qualify for these credits risk facing a penalty of up to $5,000 per return for filing a frivolous claim. Taxpayers submitting inaccurate claims also face the risk of an audit. Those who knowingly filed a false tax return also face potential criminal prosecution.

To avoid penalties and potential follow-up action by the IRS, taxpayers who incorrectly filed for these claims need to promptly submit an accurate tax return without the claims. Taxpayers can visit the IRS.gov tool Should I file an amended return? to determine if they should amend their return. If they submit an amended return, they do not need to visit an IRS Taxpayer Assistance Center. Taxpayers in this situation can also visit a trusted tax professional for advice.

The IRS noted that the entire refund amount is frozen on returns with these bad claims. Taxpayers will not receive any portion of their refund, even if they also claimed legitimate credits.

Source: IRS-2024-139, May 14, 2024