WASHINGTON — In day seven of the Dirty Dozen tax scam series, the Internal Revenue Service and Security Summit partners today alerted taxpayers to be on the lookout for unscrupulous tax preparers who could encourage people to file false tax returns and steal valuable personal information.

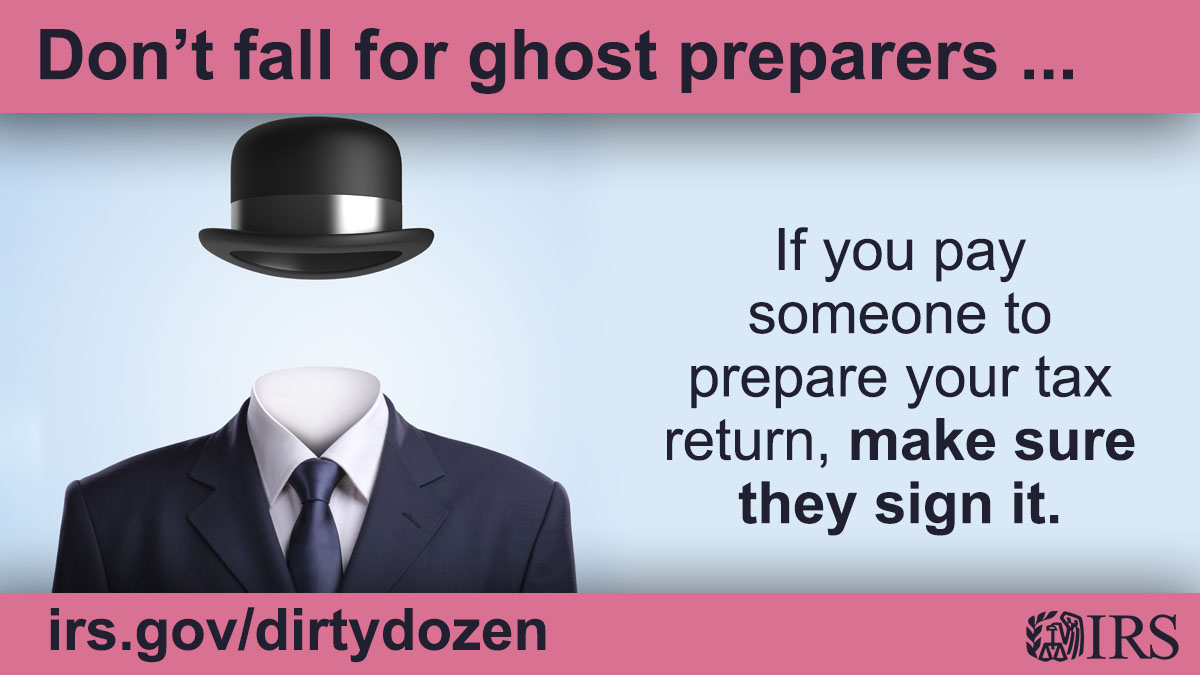

A common problem seen annually during tax season, “ghost preparers” pop up to encourage taxpayers to take advantage of tax credits and benefits for which they don’t qualify. These preparers can charge a large percentage fee of the refund or even steal the entire tax refund. After the tax return is prepared, these “ghost preparers” can simply disappear, leaving well-meaning taxpayers to deal with the consequences.

While most tax professionals offer quality service, these ghost preparers and other unscrupulous preparers try to take advantage of people and should be avoided at all costs. The IRS encourages people to use a trusted tax professional, and IRS.gov has important information to help people choose a reputable, accredited practitioner.

“Ghost preparers and other shady return preparers form a real threat every tax season to well-meaning taxpayers,” said IRS Commissioner Danny Werfel. “By trying to make a fast buck, these scammers prey on seniors and underserved communities, enticing them with bigger refunds by including bogus tax credit claims or making up income or deductions. But after the tax return is filed, these ghost preparers disappear, leaving the taxpayer to deal with consequences ranging from a stolen refund to follow-up action from the IRS. We urge people to choose a trusted tax professional that will be around if questions arise later.”

Unethical tax preparers serve as day seven of the annual IRS Dirty Dozen campaign – a list of 12 scams and schemes to help taxpayers and the tax professional community protect their personal and financial information. Compiled annually since 2002, the Dirty Dozen lists a variety of common scams that taxpayers may encounter anytime, but many of these schemes peak during filing season as people prepare their returns or hire someone to help with their taxes.

Bogus tax preparers have been a recurring theme in the Dirty Dozen for years. Anyone can file a tax return because preparing tax returns is unregulated, which adds risks for vulnerable taxpayers during filing season. To protect taxpayers, the IRS and the Treasury Department have again proposed regulating tax practitioners as part of the proposed Fiscal Year 2025 budget.

Shady tax practitioners can also be involved in stealing taxpayer identities. As a member of the Security Summit, the IRS has worked with state tax agencies and the nation’s tax industry for nine years to cooperatively implement a variety of internal security measures to protect taxpayers. The collaborative effort by the Summit partners also has focused on educating taxpayers about scams and fraudulent schemes throughout the year, which can lead to tax-related identity theft. Through initiatives like the Dirty Dozen and the Security Summit program, the IRS strives to protect taxpayers, businesses and the tax system from cyber criminals and deceptive activities that seek to extract information and money, including ghost preparers.

Tips for taxpayers: Warning signs to look out for

Most tax return preparers provide honest, high-quality service. But some may cause harm through fraud, identity theft and other scams. Paid preparers must sign and include a valid preparer tax identification number (PTIN) on every tax return. A ghost preparer is someone who doesn’t sign tax returns they prepare. These unethical tax return preparers should be avoided, especially if they refuse to sign a complete paper tax return or digital form when filing electronically.

Taxpayers are also encouraged to check the tax preparer’s credentials and qualifications to make sure they are capable of assisting with the taxpayer’s needs. The IRS offers resources for taxpayers to educate themselves on types of preparers, representation rights, as well as a Directory of Federal Tax Return Preparers with Credentials and Select Qualifications to help choose which tax preparer is the best fit.

Some of the warning signs of a bad preparer include:

- Shady fees. Taxpayers should always ask about service fees. Shady tax preparers can ask for a cash-only payment without providing a receipt. They are also known to base their fees on a percentage of the taxpayer’s refund.

- False income. Untrustworthy tax preparers may also invent false income to try to get their clients more tax credits or claim fake deductions to boost the size of the refund.

- Wrong bank account. Taxpayers should also be wary of a tax preparer attempting to convince them to deposit the taxpayer’s refund in their bank account rather than the taxpayer’s account.

Good preparers ask to see all relevant documents like receipts, records and tax forms. They also ask questions to determine the client’s total income, deductions, tax credits and other items. Taxpayers should never hire a preparer who e-files a tax return using a pay stub instead of a Form W-2. This is also against IRS e-file rules.

File accurately and check eligibility for credits and deductions

Taxpayers are ultimately responsible for all the information on their income tax return, regardless of who prepares it. Taxpayers can visit IRS.gov to find answers to tax-related questions and access tools like the Interactive Tax Assistant, which provides answers to several tax law questions specific to individual circumstances.

Filing electronically reduces tax return errors, and people can take advantage of free online and in-person tax preparation options if they qualify through programs like IRS Free File and the Volunteer Income Tax Assistance and Tax Counseling for the Elderly.

Taxpayers should also make sure that they are taking advantage of available credits and deductions, like the Earned Income Tax Credit (EITC), which is refundable and can help low-to-moderate income workers receive up to $7,340 based on their qualifications. People need to make sure they understand which credits and deductions they are eligible to claim and keep records to show their eligibility.

Report fraudulent activity and scams

The IRS highly encourages people to report tax return preparers who deliberately prepare improper returns and any activity that promotes improper and abusive tax schemes.

To report an abusive tax scheme or a tax return preparer, people should use the online Form 14242 – Report Suspected Abusive Tax Promotions or Preparers, or mail or fax a completed Form 14242PDF and any supporting material to the IRS Lead Development Center in the Office of Promoter Investigations.

Mail:

Internal Revenue Service Lead Development Center

Stop MS5040

24000 Avila Road

Laguna Niguel, CA 92677-3405

Fax: 877-477-9135

Taxpayers can also report preparer misconduct using Form 14157, Complaint: Tax Return PreparerPDF. If a taxpayer suspects a preparer filed or changed their tax return without their consent, they should file Form 14157-A, Tax Return Preparer Fraud or Misconduct AffidavitPDF.

Alternatively, taxpayers and tax practitioners may send the information to the IRS Whistleblower Office for possible monetary award.

Source: IRS-2024-96, April, 2024